CBSE Class 12th Accountancy Syllabus 2023

Syllabus for CBSE Class 12 Accountancy 2022-2023: Check out and download the new CBSE Class 12 Accountancy syllabus for the 2022-2023 school year. Examine the entire syllabus to learn about the chapter-by-chapter subjects to prepare for the forthcoming board test. This syllabus also includes a unit-wise marks breakdown to help with topic division based on high and low weightage.

Skip to

Download the CBSE Class 12th syllabus of accountancy

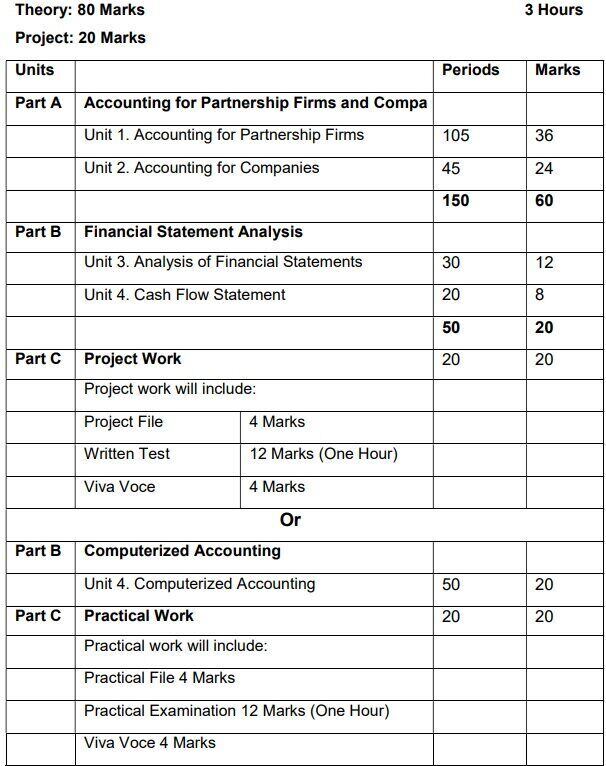

Part A: Accounting for Partnership Firms and Companies

Unit 1: Accounting for Partnership Firms

|

Units/Topics |

Learning Outcomes |

Note: Interest on partner's loan is to be treated as a charge against profits. Goodwill: meaning, factors affecting, need for valuation, methods for calculation (average profits, super profits and capitalization) , adjusted through partners capital/ current account or by raising and writing off goodwill (AS 26) Accounting for Partnership firms - Reconstitution and Dissolution. ·

Note: (i) If the realized value of tangible assets is not given it should be considered as realized at book value itself. (ii) If the realized value of intangible assets is not given it should be considered as nil (zero value). (iii) In case, the realization expenses are borne by a partner, clear indication should be given regarding the payment thereof. |

After going through this Unit, the students will be able to: ·

|

Conclusion

Some tips to score well in the CBSE Class 12 Accountancy exam are to focus on understanding the concepts, practice solving different types of problems, create summary notes, and revise regularly. Additionally, reading the question paper carefully and managing time effectively can also help in scoring well

FAQs

Q: What are the topics covered in the CBSE Class 12 Accountancy syllabus?

A: The CBSE Class 12 Accountancy syllabus covers topics such as Accounting for Partnership Firms, Reconstitution and Dissolution, Accounting for Companies, Analysis of Financial Statements, Cash Flow Statement, and more.

Q: What is the duration of the CBSE Class 12 Accountancy exam?

A: The CBSE Class 12 Accountancy exam is of three hours duration.

Q: What is the maximum marks for the CBSE Class 12 Accountancy exam?

A: The maximum marks for the CBSE Class 12 Accountancy exam is 80.

Q: What is the minimum passing marks for the CBSE Class 12 Accountancy exam?.

A: The minimum passing marks for the CBSE Class 12 Accountancy exam is 33%.

Download CBSE Syllabus of class 12th Accountancy

MissionGyan Team

We aim to eradicate the education gap and serve equal and free education to all with the help of skilled and expert volunteers and teachers.

Nice blog! Is your tһeme custom made or did you download it from somewhere?

A design like youгs with а few simple adjustements wouⅼd rеallу make my blog stand out.

Ρlease let me know where you got your theme. Κudos